Group Insurance Health Screening vs Individual Underwriting: Key Differences

Group insurance health screening vs individual underwriting: a research-based look at how data collection, pricing, and enrollment differ across insurance models.

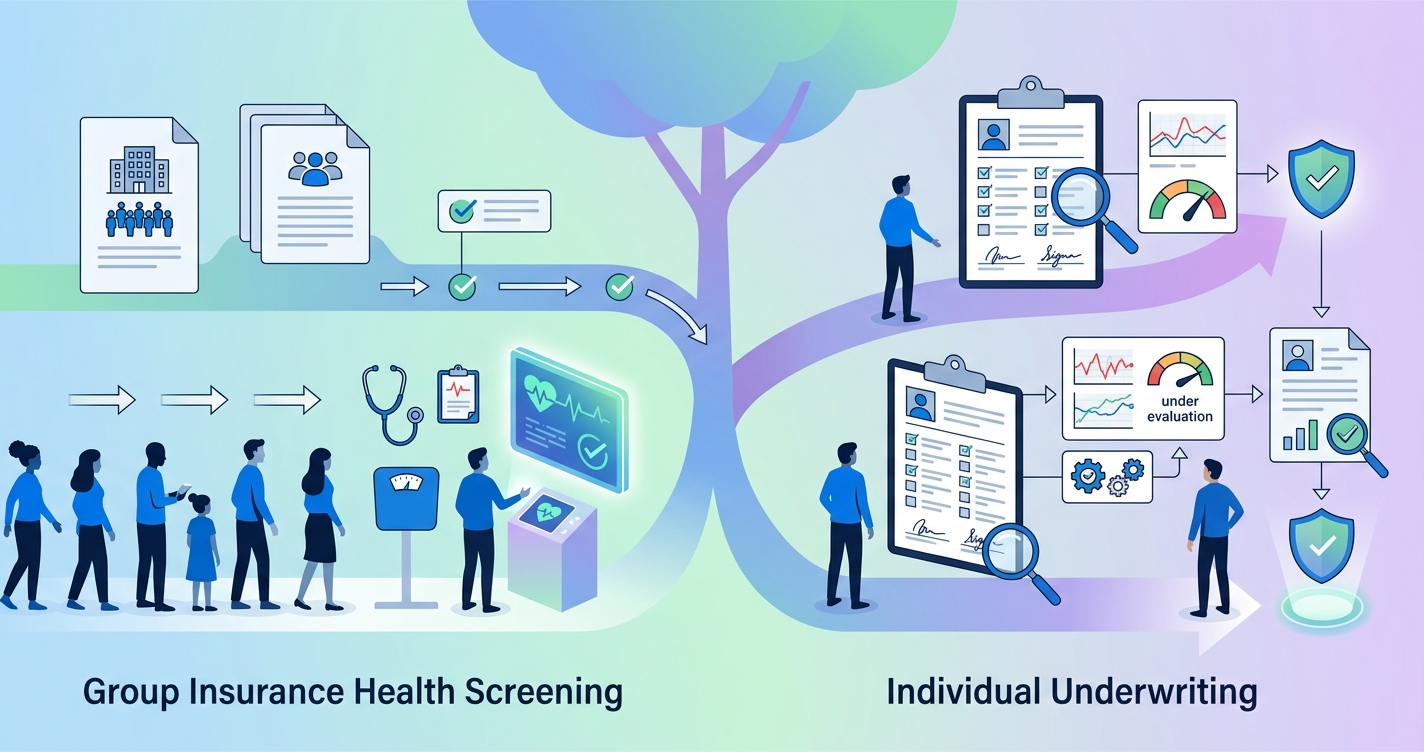

Group insurance health screening vs individual underwriting is really a question about scale. In a group setting, carriers and administrators usually want signals about a population: who is eligible, where risk is concentrated, and how screening can fit inside enrollment or wellness workflows without slowing everything down. Individual underwriting works differently. It is built around one applicant at a time, one file at a time, and a much narrower decision: should this person be issued coverage, and on what terms?

"Fewer than half of employees (46 percent) in the firms surveyed undergo clinical screening or complete a health risk assessment." - Soeren Mattke and colleagues at RAND, Workplace Wellness Programs Study: Final Report (2013)

Group insurance health screening vs individual underwriting in practice

The operational gap starts with the unit of analysis. Group insurance screening is usually tied to an employer, association, or enrollment cohort. The goal is often to support wellness program design, population risk segmentation, incentive eligibility, or smoother enrollment operations. The NAIC's Group Health Insurance Standards Model Act defines "evidence of individual insurability" as health information used to limit or exclude coverage, but its HIPAA-era drafting notes also point to rules that restrict health-status-based eligibility barriers in group coverage. That matters because group workflows typically collect health data inside a broader framework of eligibility and program administration, not pure case-by-case medical selection.

Individual underwriting, by contrast, is designed to evaluate a single person directly. The underwriting file may include questionnaires, medical history, pharmacy data, labs, or an exam depending on the product and market. The NAIC's consumer guidance on individual health insurance frames this market around direct purchase by people and families rather than employer sponsorship. In plain terms, the insurer is not looking at an employee population. It is looking at one applicant and deciding how much uncertainty it can tolerate.

That difference changes almost everything downstream: the data requested, the timing, the compliance posture, and the economics of the workflow.

Comparison table: group screening versus individual underwriting

| Dimension | Group insurance health screening | Individual underwriting |

|---|---|---|

| Primary purpose | Population-level screening, enrollment support, wellness qualification, risk segmentation | Applicant-level selection and pricing |

| Unit of review | Employer group, class, or enrolled cohort | Single applicant |

| Timing | Often during enrollment cycles or wellness campaigns | At application or policy issue |

| Data collection style | Standardized screening across many participants | Customized file review based on one person's risk profile |

| Decision output | Program eligibility, incentives, population insights, operational triage | Approve, rate, postpone, or decline depending on product rules |

| Operational priority | Speed, participation, and scalability | Precision per applicant |

| Compliance focus | HIPAA, workplace privacy, employer/firewall issues, state biometric rules | Consumer disclosure, adverse action rules, product-specific underwriting controls |

| Buyer concern | Participation rates, admin burden, usable aggregate data | Accuracy of individual risk assessment and turnaround time |

For carriers, TPAs, and consultants, that table is more than theory. It explains why the same screening technology can feel seamless in a group enrollment pilot and painfully slow if someone tries to force it into an individual underwriting process it was never built to match.

Why group insurance health screening is built for throughput

The KFF 2025 Employer Health Benefits Survey offers a useful reality check. Family premiums in employer-sponsored coverage reached $26,993, and 43% of larger firms offered workers the opportunity to complete a biometric screening. Among large firms with a biometric screening program, 62% used incentives or penalties to encourage completion. Those numbers tell you two things.

- Screening is already part of the employer-sponsored landscape.

- Participation and workflow design still determine whether a program is useful.

In group insurance, the buyer rarely asks for a perfect portrait of every covered life. The buyer wants a process that can work across thousands of members during a compressed enrollment window. That pushes screening toward standardized intake, easier digital completion, and clean data transfer into enrollment and care-management systems.

RAND's 2013 wellness study, led by Soeren Mattke with Harry H. Liu, John P. Caloyeras, Christina Y. Huang, Kristin R. Van Busum, Dmitry Khodyakov, and Victoria Shier, found that incentives matter: every $10 increase in HRA incentives was associated with a 1.6 percentage point increase in completion rates within the studied range. For group insurance operators, that is a workflow lesson as much as a wellness finding. Participation is not just about employee motivation. It is about how the process is designed.

This is one reason digital-first screening keeps gaining ground in employer settings. Saeed Amirabdolahian, Guy Pare, and Stefan Tams of HEC Montreal wrote in their 2025 Journal of Medical Internet Research meta-review that digital wellness programs show broad promise in efficacy and acceptability across workplace health domains. That does not mean every platform works equally well. It does mean digital delivery is no longer a fringe idea. It is part of the mainstream operating model for programs that need reach and consistency.

Where individual underwriting still differs sharply

Individual underwriting has a different tolerance for ambiguity. The insurer is not asking, "How do we screen this population efficiently?" It is asking, "What do we know about this applicant, and is that enough to issue coverage under our rules?"

That shift has several consequences.

- The data trail is more individualized and often more invasive.

- Turnaround time depends on whether extra evidence is needed.

- Exceptions matter more because each case can change pricing or eligibility.

- The workflow is less forgiving of missing or inconsistent information.

Even when digital tools shorten the process, the logic remains applicant-specific. A group carrier can still get value from aggregate health signals, participation data, and trend analysis. An individual underwriter usually needs enough evidence to support a decision on one person, not a population trend.

This distinction also affects how stakeholders evaluate success. In a group screening program, a consultant may care most about completion rates, employer satisfaction, and whether data arrives in time for open enrollment. In individual underwriting, the success metric is more likely to be decision confidence, case placement rate, or reduction in manual follow-up.

Industry applications for carriers, TPAs, and consultants

Carrier operations

Group carriers use screening to understand a book of business, align wellness incentives, and improve enrollment flow. That makes a scalable intake model more valuable than a highly customized case review model. Individual lines need the opposite: strong file assembly and decision support at the applicant level.

TPA administration

TPAs often sit closest to the operational pain. In group programs, they have to coordinate communications, completion tracking, data handoff, and employer reporting. Standardization matters because the administrator may be managing many employer groups at once. That is very different from an individual case desk where each file can branch into its own evidence path.

Benefits consulting

Consultants advising employer clients usually need screening programs that are easy to explain and easy to launch. They are less interested in fine-grained applicant selection than in whether a screening model can support open enrollment, wellness strategy, and year-round engagement. That is why posts like How to Run Biometric Screening for Group Insurance Enrollment and Digital Screening Reduces Group Underwriting Costs keep resurfacing in RFP conversations: the operational questions are practical, not abstract.

Current research and evidence

The strongest evidence base around group screening still comes from employer wellness and enrollment research rather than classic underwriting literature. That is worth saying plainly. The market talks about "underwriting" all the time, but much of the measurable evidence is really about participation, digital engagement, and program design.

RAND found that workplace wellness participation remained limited overall, with fewer than half of employees in surveyed firms completing clinical screening or HRAs. KFF's 2025 survey shows biometric screening remains common among larger employers, but not universal. Together, those findings suggest the core challenge in group insurance is not whether health screening exists. It is whether the process is convenient enough to produce usable data at scale.

The HEC Montreal meta-review adds another layer. Across 29 qualifying reviews published between 2000 and 2023, digital wellness programs generally showed acceptable engagement and promising efficacy, though the authors also noted gaps around durability and causal mechanisms. That is a useful caution for insurance buyers. Digital delivery improves access and scalability, but it does not eliminate the need for careful program design, privacy controls, and realistic expectations.

The NAIC material helps frame the compliance side. Group coverage rules and individual coverage rules are not interchangeable. Once screening moves into employer-sponsored settings, privacy boundaries, incentive design, and the separation between employment decisions and health data become central. In individual underwriting, the compliance center of gravity shifts toward applicant disclosure, product rules, and the defensibility of case-level decisions.

The future of group insurance health screening

The next phase is unlikely to erase the line between group screening and individual underwriting. If anything, the line may get clearer.

Group programs are moving toward faster digital intake, better participation analytics, and tighter integration with enrollment systems. Individual underwriting is moving toward faster evidence gathering too, but it still revolves around one insured life at a time. Those are related paths, not identical ones.

For insurance organizations, the practical question is not which model is better in the abstract. It is which model fits the product, the buyer, and the workflow. A group enrollment team needs reach, consistency, and low friction. An individual underwriting team needs defensible applicant-level evidence. Confusing one for the other usually creates extra work, not innovation.

Frequently asked questions

Is group insurance health screening the same as medical underwriting?

No. Group insurance health screening is often used for enrollment support, wellness qualification, or population risk analysis. Medical underwriting usually refers to a case-level decision on an individual applicant.

Why do group insurance programs emphasize participation so much?

Because the value of a group screening program depends on enough members completing the process to make the data operationally useful. RAND's findings on incentives and completion rates show that design choices directly affect that outcome.

Does digital screening replace individual underwriting?

Usually not. It can improve intake and reduce friction, but individual underwriting still depends on applicant-level evidence and product-specific rules.

Who cares most about the difference between these two models?

Group carriers, TPA administrators, and benefits consultants do. They need to know whether they are buying a screening workflow for population operations or a process built for one-by-one underwriting decisions.

Insurance teams exploring scalable screening models for enrollment and wellness programs can see how Circadify is approaching this category at Circadify's payer and insurance solutions.