Phone Scan vs Lab Test for Group Life Health Data

Comparing 60-second phone scans against traditional blood draws for group life underwriting health data, with cost, speed, and participation evidence for carriers.

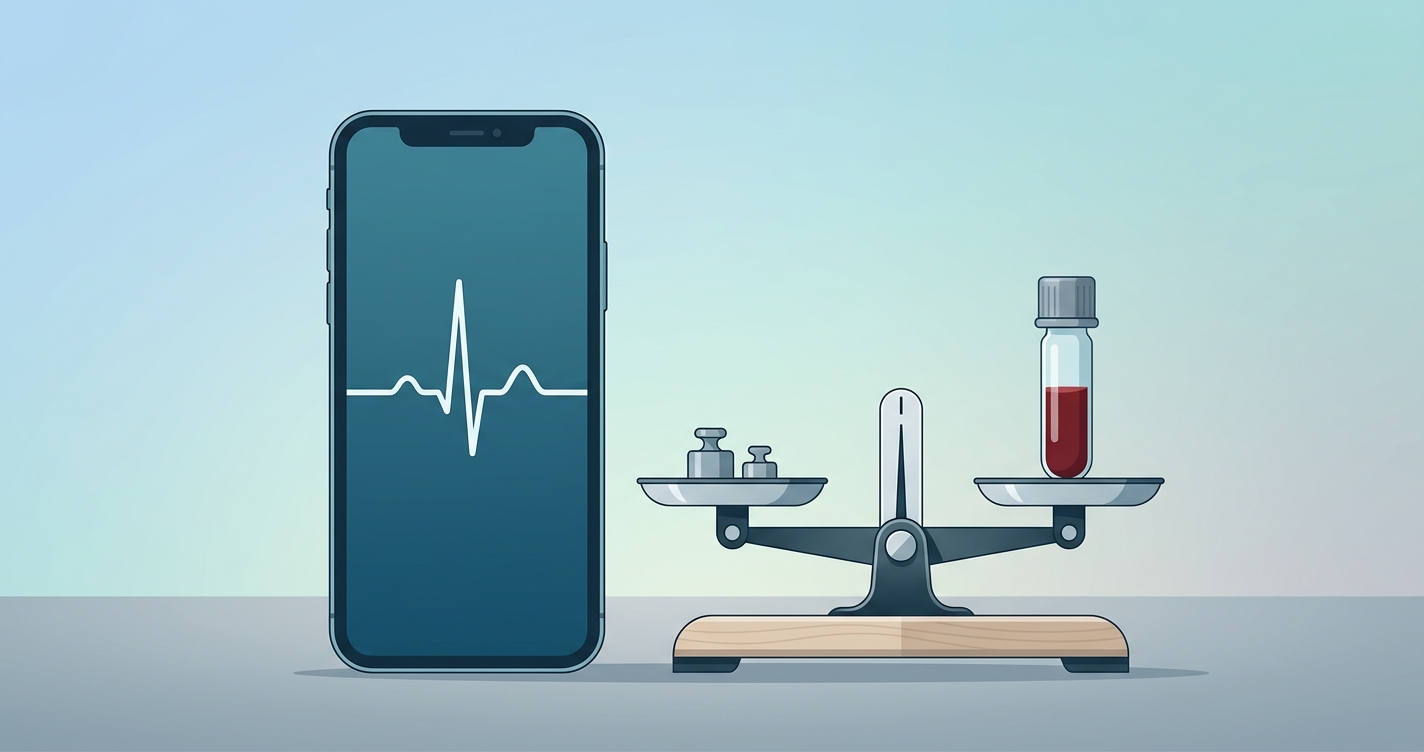

Group life carriers have spent decades treating the blood draw as the price of admission for any meaningful health signal. That assumption is now under pressure. A 60-second smartphone scan can capture a useful slice of group life underwriting health data without a phlebotomist, a lab courier, or the two-week wait that quietly kills enrollment momentum. The question facing carriers, TPA administrators, and benefits consultants is no longer whether digital intake works, but where it earns its place against the lab test and where the lab still wins.

"An average of 59% of individual life applications now qualify for an accelerated underwriting path, with over 60% of life insurers investing in simplified and accelerated systems," reports Gen Re in its 2025 U.S. Individual Life Next Gen Underwriting Survey.

That migration away from fluid-dependent evidence is the backdrop for every group life data decision being made right now.

Reframing group life underwriting health data collection

The traditional paramedical exam was built for one-at-a-time individual underwriting, not for enrolling a 4,000-life employer group in a three-week open enrollment window. When carriers try to scale blood draws across a worksite, the friction compounds: scheduling, fasting requirements, lab logistics, and abandonment all rise with headcount. A phone scan inverts that math. It collects group life health data at the moment of enrollment, on a device the employee already owns, with no facility to book.

The relevant technology is camera-based photoplethysmography (PPG), which reads subtle color changes in the skin to estimate cardiovascular and metabolic signals. The same family of optical signals that drives wrist wearables can be captured through a phone camera. What changes between a phone scan and a lab test is not just convenience but the type of signal and the population coverage it produces.

Here is how the two intake methods compare across the dimensions that matter to a group life underwriter.

| Dimension | 60-Second Phone Scan | Traditional Lab Test (Blood Draw) |

|---|---|---|

| Time to result | Seconds to minutes | 7 to 14 days typical |

| Per-life cost | Low marginal cost, software-based | $75 to $150+ per exam including logistics |

| Participation friction | Self-serve, no appointment | Scheduling, fasting, facility visit |

| Population coverage | High, scales with the whole group | Low, often limited to large face amounts |

| Signal type | Cardiovascular, metabolic estimates, vitals | Lipids, glucose, cotinine, biomarkers |

| Invasiveness | Non-invasive, contactless | Venipuncture |

| Best fit | Broad group screening, voluntary tiers | High face amount, individual confirmation |

| Repeatability | Easy annual or quarterly re-scan | Costly to repeat at scale |

The table makes the strategic split obvious. A blood draw produces a deeper, lab-grade biomarker panel for a single life. A phone scan produces a shallower but far broader dataset across an entire enrolled population. For group life, where the underwriting goal is signal across the pool rather than forensic detail on one applicant, breadth often carries more value than depth.

Carriers weighing a lab test alternative should keep a few realities in view:

- Coverage beats precision at the group level. A signal captured on 85% of a group informs pricing more than a lab-grade reading captured on 12%.

- Participation is the hidden variable. Every percentage point of abandonment shrinks the risk picture and skews it toward the healthy and motivated.

- Re-measurement matters. Phone scans can be repeated cheaply each enrollment cycle, turning a one-time snapshot into a trend.

- The two methods are not mutually exclusive. Many carriers reserve fluids for high face amounts and use digital intake everywhere else.

Industry applications for digital health data for life coverage

The comparison stops being abstract once it is mapped to specific group life workflows. Three applications are moving fastest.

Guaranteed issue and voluntary buy-up tiers

Group life often sits on a guaranteed issue base with voluntary buy-up layers that historically triggered evidence of insurability. Phone scans let carriers gather digital health data for life coverage at the buy-up boundary without forcing a blood draw, smoothing the step-up experience and widening the population that completes the higher tier.

Open enrollment population capture

Open enrollment is the single largest data-collection event in employer benefits, yet most carriers let it pass with only census data. Embedding a scan into the enrollment flow converts that window into a population-health intake moment, producing group life underwriting health data that also feeds wellness and stop-loss conversations.

Re-underwriting and renewal pricing

Because a scan is cheap to repeat, carriers can re-measure a group at renewal rather than relying on stale evidence. That creates a longitudinal view of pool health that a one-time blood draw can never deliver at scale.

Current research and evidence

The scientific base for optical, camera-derived health signals has strengthened sharply. In June 2024, a team publishing in PLOS Global Public Health described a deep-learning PPG-based cardiovascular risk score that predicted ten-year major adverse cardiovascular events using only age, sex, smoking status, and a PPG waveform. Google Research published parallel work in July 2024 on predicting cardiovascular disease risk from fingertip and smartphone PPG signals combined with deep learning, framing it as a path toward heart-health screening for billions.

Validation for specific vitals is also maturing. An April 2024 study in EP Europace (Oxford Academic) validated smartphone-based PPG for rate and rhythm monitoring in atrial fibrillation under real-world conditions. On the blood pressure front, Lifelight received Class II medical certification in June 2025 for measuring blood pressure using remote PPG from a phone camera, an early regulatory marker for contactless intake.

The literature is candid about limits. A March 2025 review noted that while smartphone PPG offers a low-cost route to continuous blood pressure estimation, current models still face challenges meeting established measurement standards for general use. The honest reading for a group life underwriter: phone scans are strong for population-level risk stratification and screening, while lab fluids remain the reference for confirmatory, biomarker-specific evidence on individual high-value lives. That division of labor, rather than a winner-take-all outcome, is what the evidence supports today.

The future of group life health data collection

Three trends will define the next several renewal cycles. First, accelerated underwriting will keep expanding, and with Gen Re reporting more than 60% of life insurers investing in simplified systems, the fluidless default is becoming the industry norm rather than the exception. Second, the signal set captured by a phone will widen as optical models add blood pressure, respiratory, and metabolic estimates that carry regulatory recognition. Third, carriers will increasingly run hybrid intake: a universal phone scan across the group, with reflexive fluids triggered only when face amount or flagged signals justify the cost.

The strategic implication is that the lab test is not disappearing so much as being repositioned. It becomes a targeted confirmatory tool rather than the default front door. The front door, for the bulk of a group, becomes a scan that any employee can complete in under a minute. Carriers that design for that split now will hold cleaner, broader, and more current group life data than those still gating every signal behind a blood draw.

Frequently asked questions

Can a phone scan replace a blood draw entirely for group life underwriting? Not entirely, and that is rarely the goal. A phone scan captures broad cardiovascular and metabolic signals across an entire group, while a blood draw delivers lab-grade biomarkers on individual lives. Most carriers use scans as the default intake and reserve fluids for high face amounts or flagged cases.

What kind of health data does a 60-second scan actually produce? Camera-based PPG scans estimate cardiovascular and vital-sign signals such as heart rate and, in newer validated systems, blood pressure. They do not produce lipid panels, glucose, or cotinine values, which still require a fluid sample.

Why does participation matter more than precision for group life? Group underwriting prices a pool, not a person. A signal captured across most of a group gives a more representative risk picture than a precise reading collected on a small, self-selected minority. Higher participation reduces the bias that comes from only the healthiest employees completing intake.

Is digital health data for life coverage credible enough for pricing? For population-level stratification and screening, peer-reviewed work from 2024 and 2025 supports the use of PPG-derived risk signals. For confirmatory, biomarker-specific evidence on individual high-value lives, lab fluids remain the reference standard.

Circadify is building scalable biometric screening for exactly this group life intake problem, pairing 60-second phone scans with the population-coverage carriers need at enrollment. Group insurance carriers and TPAs evaluating a lab test alternative can explore the enterprise pilot program at circadify.com/industries/payers-insurance to test digital intake against their current underwriting workflow.